Is Working with Your Advisor Worth It?

There has always been a collective of individuals out there who feel managing their wealth independently is the best way to go. These individuals’ main argument is they don’t want to pay an advisor because they don’t see the “real value.” Unfortunately, here at DLAK, we have been preaching a similar idea. Not because there’s no value in working with an advisor, but because most advisors DON’T provide the value they should.

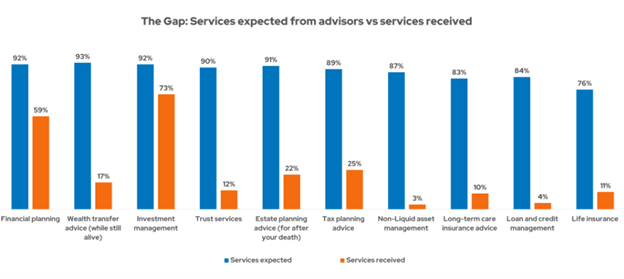

Since founding the firm 20 years ago, Rob has made it his mission to deliver the highest level of service to every client. In 2022, while attending a conference in Phoenix, he came across a powerful graphic that reinforced this troubling truth: despite investors expecting more holistic guidance, a 2021 Spectrum Group study revealed most advisors still fall short of providing it.

Source: Spectrem August 2021 Defining Wealth Management

Neither Envestnet, Envestnet | PMC nor its representatives render tax, accounting or legal advice.

Advisors today are doing too little and getting paid too much!

At DLAK, we are changing the script. We ensure every aspect of your financial life is covered, including all areas noted in the Spectrum study. For more than two decades, our mission has been to provide a comprehensive suite of services, including investment management, protection planning, financial planning, gifting and philanthropy, and wealth transfer strategies.

So now, let’s take a look at four simple, straightforward examples that highlight the real value you receive by working with a DLAK Advisor, compared to the industry standard.

Example #1: Trading Frequency

Though there is wide variation, the average actively managed portfolio has a turnover rate of roughly 80% per year—a clear sign of how frequently many investors trade. To illustrate the impact of this, let’s consider a hypothetical investor with the following baseline assumptions: (source:icfs.com)

- Taxable account value: $500,000

- Annual turnover: 80%

- Annual capital gains: $20,000

- All short-term gains taxed at a 22% marginal rate

This hypothetical investor would pay roughly $88,000 in taxes over a 20-year period just because they frequently traded their brokerage account.

Had this investor worked with DLAK, they would have learned that frequent trading doesn’t belong in a taxable account. Instead, they’d keep higher-turnover strategies in an IRA or Roth IRA and manage the brokerage account more efficiently. By reducing turnover to 10% and realizing only $2,500 in long-term capital gains per year, taxes over 20 years could drop to around $7,500.

Over 20 years, a smart, tax-efficient advisor could have potentially saved this client $80,500 in taxes.

Example #2: Retirement Asset Location

Understanding the difference between certain types of tax registrations (Traditional IRA, Roth IRA, Taxable Brokerage Account, etc.) could save clients hundreds of thousands of dollars over their lifetime. A traditional IRA uses pre-tax money, grows tax-deferred, and is taxed on withdrawal, while a Roth IRA uses after-tax money and grows and qualified withdraws are income tax-free.

Consider a 40-year-old client with $500,000 in a Traditional IRA and a Roth IRA. Both accounts are allocated 50% stocks and 50% bonds. The individual pays a total effective tax rate of 28% tax, earning 6% annually (assuming stocks return 9%/year & bonds yield 3%/year). Without tax-aware planning, they’d end up with ~3.7 million in after tax, spendable dollars.

With DLAK’s guidance, allocations are adjusted: typically the Roth is 100% stocks, the traditional IRA 0% stocks (keeping the overall risk level the same – 50/50). Assuming the same market returns as above, the individual would end up with roughly $4.05 million over that same 25-year period.

A potential savings of over $310,000!

Example #3: Social Security Maximization

Many people view their Social Security benefit as an individual benefit taken independently of the other spouse. In some cases that may be true (if you are single, spouse passes away, etc.), but for most MFJ (married filing jointly) couples the benefit needs to be looked at differently.

Given the example below, let’s look at how maximizing Social Security could help make you hundreds of thousands of dollars better off over your lifetime.

- Spouse 1 is 62 years old and has a full retirement age (FRA) benefit of $45,000 per year.

- Spouse 2 is 60 years old with an FRA benefit of $25,000 per year.

In this example, we will compare three scenarios:

- Both take at 62 – as soon as possible

- Both take at FRA (67) – when you get full benefit

- Maximization - The younger spouse takes their smaller benefit at 62 and the other spouse delays the higher benefit till 70

Scenario 1: If the couple ignores a joint benefit strategy and both spouses claim their Social Security benefits as soon as they are eligible, the results can be costly. Assuming one spouse passes away at the normal individual life expectancy of 80, while the surviving spouse lives until the joint life expectancy of 90, the couple would receive a total of $1.588 million in benefits from the government.

Scenario 2: If both spouses wait to claim their full Social Security benefits at their full retirement age of 67, and assuming the same life expectancy assumptions as in Scenario 1, the couple would receive a total of $1.834 million in benefits from the government.

Scenario 3: By maximizing their benefits—having the younger spouse claim their smaller benefit at 62 while delaying the higher benefit until age 70, which increases it by 8% for each year delayed between 67 and 70—the couple, assuming the same life expectancy assumptions as in Scenarios 1 and 2, would receive a total of $1.88 million in benefits from the government.

By thinking about Social Security as a joint benefit and using the maximization strategy, this client ended up $300,000 better off than if they had claimed benefits immediately and $50,000 better off than if they had waited until full retirement age.

Example #4: Charitable Gifting Strategies

Gift Bundling – At our firm, we have access to several options one being a Donor-Advised Funds (DAFs) to help clients manage taxes during high-income years. By contributing a portion of a bonus, business sale, or investment gain to a DAF, clients receive an immediate tax deduction, lowering their taxable income. The funds can then be donated to charities over time, allowing clients to smooth income spikes, stay in lower tax brackets, and preserve more after-tax wealth while supporting the causes they care about.

Consider a couple in the 24% tax bracket that typically takes the $31,500 standard deduction each year. They normally have $10,000 in SALT taxes, $10,000 in mortgage interest, and give $10,000 to charity ($30k total of itemized deductions - still below the standard deduction threshold). This person gets ZERO benefit for the $10,000 they gave, because they end up taking the standard deduction and not getting to write off the gift as they would had they itemized.

If this person instead bundles their giving using a donor-advised fund (DAF), they could give 3 years' worth of charitable contribution ($30,000) and take the tax deduction all in one year. With a charitable deduction of $30,000, SALT of $10,000, and mortgage interest of $10,000, the total itemization would now be $50,000 — more than the standard deduction. Now, the individual gets to write off $18,500 ($50,000 itemizations - $31,500 standard deduction) of their charitable gift. That is roughly $6,167 of extra tax deferment each year.

At a tax rate of 24%, this individual would get an extra tax break of $4,440 every 3 years. Over a 20-year period, this strategy could result in savings of approximately $30,000.

Conclusion

Financial outcomes depend on coordinating taxes, account allocation, spending, and charitable planning — not just picking investments. While individuals may be able to attend to one or two of these areas while balancing a full-time job, by working with the RIGHT ADVISOR, you could have the ability to take advantage of all of these strategies and more.

When you combine all the savings outlined above, an individual could pocket a staggering $600k roughly over 20 years — an extra $30,000 per year in your hands! Imagine a $2 million investment portfolio paying a 1.00% advisory fee — $20,000 per year. By simply implementing these four strategies, not only could you cover your advisory fee, but you’d still walk away with over $10,000 extra in your pocket every year.

Paying an advisor to do nothing doesn’t make sense, but paying the RIGHT advisor could save you millions over your lifetime.